~ ASPN, Zilch’s proprietary ad-sales platform, achieves conversion rates of up to 55%, surpassing the search industry average by 10+ times – enabling the Googlisation of Payments ~

~ The Ad-Subsidised-Payments-Network allows retailers to offer contextualised advertising deals directly to customers through its vertically integrated payments app

~ Platform brands such as Amazon and Ebay achieve average conversions of 59% ~

~ Food & Drink sector witnessed particularly outstanding results, with brands achieving an average conversion rate of c.70% ~

~ Significantly reduced product return rates across all sectors, averaging just 7% compared to the typical ecommerce range of 20-30% ~

Zilch, the pioneering direct-to-consumer (D2C) payments technology and advertising platform, is today announcing the official rollout of its Ad-Subsidised-Payments-Network (ASPN) to third parties through open APIs. The proprietary ad-sales platform has demonstrated unprecedented performance, delivering outstanding results for retailer partners and, more importantly, providing customers with over $160 million in savings via cashback, rewards and interest-free credit.

Zilch initially created ASPN to power its own ad-subsidised Buy Now Pay Later (BNPL) product offering, attracting over 3 million registered customers in just 24 months and seeing more than 5,000 retailers reallocate their advertising spend away from clicks and impressions to a payments platform that only charges for sales. With more than $1.7 billion in commerce having been transacted through the platform, ASPN is now being made available through open APIs to any third-party app / card issuer that wants to participate in the network, which is already integrated with 38 million merchants worldwide. Partners can access the network of dynamic commissions through APIs which provide new revenue streams outside of interchange. Merchants can adjust these commissions and attribute sales (online and offline) in real time without any change to their existing payment infrastructure.

The democratisation of access to Zilch’s ASPN will create new business-to-business revenue for the firm and substantial additional revenue opportunities for partners, all while accelerating Zilch’s mission: to eliminate the cost of consumer credit (using ad subsidies), for good.

The unparalleled performance of Zilch’s ASPN platform demonstrates the power of retail media, helping Zilch become a game-changer in today’s fintech industry. An analysis of the data from ASPN’s performance shows:

- Brands can achieve a conversion rate (the proportion of customers who make a purchase after interacting with the advert) of up to 55% – significantly higher than the industry averages for traditional forms of digital advertising that range from c.2% to 10%.

- Food and drink brands are converting at an average of c.70% of ad interactions into sales. Brands such as Amazon achieve average conversions of nearly 60%.

- Retailers also saw product return rates plummet, averaging 7% across all sectors compared to the average e-commerce range of 20-30%. This shows how Zilch helps retailers reach customers with a genuine intent to buy rather than stoking impulse purchases, which is hugely beneficial to both the retailer and the consumer (not to mention the environment too).

- Zilch’s current top 30 merchant partners alone generate a combined $700 billion of revenue annually and pay an average commission to Zilch of over 6% on each purchase made via the Zilch platform. That speaks to the commercial opportunity for Zilch and its new retail partners as well as the scalability of this unique business model.

Philip Belamant, CEO and Co-Founder of Zilch, said: “Our vision with Zilch was to offer all customers an incredible payments product that would eliminate the cost of consumer credit for good. To achieve this, we generate ad revenue from merchants when customers shop and use this to subsidise our powerful reward-earning debit and zero-interest credit in one digital card that customers can use anywhere. This is what we call the Googlisation of Payments. Uniquely, merchants can redirect ad spend to Zilch away from clicks and impressions on traditional platforms that suffer fraud, lack of attribution and don’t necessarily convert into sales.

“Opening up ASPN to third parties is an important step in creating what could be a trillion-dollar-plus payments ad-marketplace. On one side you will have millions of consumers transacting billions every month and receiving access to interest-free-credit, savings and rewards on their purchases. On the other, you’ll have hundreds of thousands of retailers bidding to get in front of a massive closed-loop network of ultra-high-intent consumers with a sustainable means to spend.

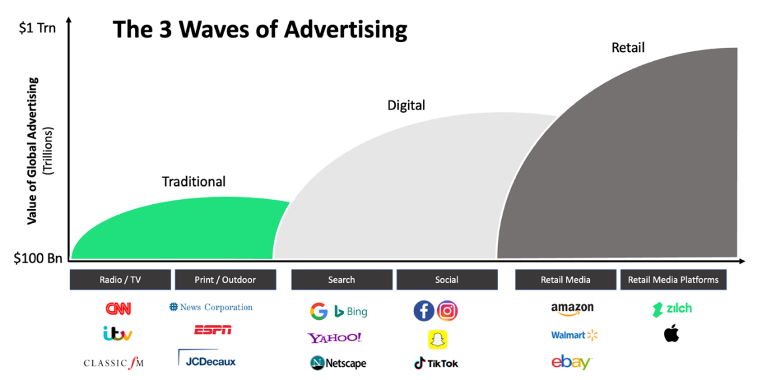

“We truly believe that this is the future of the advertising industry, and that our current results, across almost $2 billion of commerce to date, bear evidence to that. The market continues to see a decline in spend on search and social media advertising in favour of retail media, where retailers sell online ads using their first-party data, precisely because retail media provides advertisers with better targeting at times of maximum ‘intent’, higher conversion and more accurate attribution. What data from ASPN shows is that, when you place those ads on a consumer’s favourite payments platform and enable them to make the purchase, rather than on the checkout page of an ecommerce site, the performance is unparalleled.”

Click here to register for our white paper, coming soon.